The Crypto Clarity Act - As Clear as Mud

In this article:

According to politicians, regulators, and suitcoiners, the rules of engagement in the crypto industry aren’t clear enough, and without their wise stewardship, all hell would break loose.

Thank God they’re here to protect us!

That’s why you’ll have heard a lot of noise recently about the Crypto Clarity Act, a bipartisan bill which aims to create a clearer regulatory environment for the cryptocurrency industry and safeguard consumers.

Proponents claim the bill will allow US crypto businesses to innovate without fear of regulation through enforcement, while protecting consumers from drug-addled scammers like Sam Bankman-Fried, who would otherwise commingle and gamble away their funds.

Taken at face value, these seem like noble aims. After all, the FTX debacle cost investors millions of dollars, and the Wild West nature of the crypto industry facilitates an endless cycle of scam tokens, insider trading, and rug pulls. In the absence of proper regulation, people can brazenly launch worthless shitcoins and scam people out of their hard-earned money without consequence.

Isn’t it about time the government stepped in and put a stop to this madness?

Well, you probably shouldn’t hold your breath…

If you were hoping the Clarity Act would provide clarity, you were sadly mistaken. Despite having been introduced to the House of Representatives almost eight months ago, the stakeholders involved still can’t reach agreement on what the rules should be.

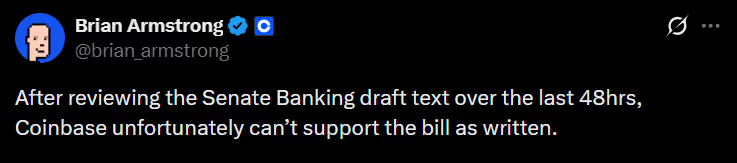

The bill passed the House of Representatives in July 2025 with broad support, but progress came to an abrupt halt recently when Coinbase CEO Brian Armstrong announced on X that the company could no longer back the Senate Banking Committee’s draft, stating, “We’d rather have no bill than a bad bill.”

So, what exactly is this bill? And if it’s meant to deliver regulatory clarity for the crypto industry, then why is it a tedious 278 pages long? Satoshi’s white paper manages to outline Bitcoin’s entire design in just nine.

Perhaps it’s because Congress doesn’t really understand what it’s doing…

This week, let’s explore the Clarity Act in more depth to try to understand what it contains, what the implications are, and why people are getting so animated about it.

What Is the Clarity Act?

Don’t worry, we’re not going to walk through the entire 278-page bill. Instead, let’s break it down into its core components to make better sense of what we’re dealing with.

There are four key focus areas of the bill:

1) Who Regulates What

For a long time, the crypto industry has seen the Securities and Exchange Commission (SEC) as an adversary, and the former chair, Gary Gensler, was often painted as the villain.

Industry players complained that a lack of clear guidelines made it tricky to determine whether their projects would be classified as securities, forcing many to operate in legal limbo and driving “innovation” into the shadows.

(Most would prefer not to be classified as securities to avoid scrutiny from the SEC).

The Clarity Act seeks to resolve this by making a clear distinction between different types of crypto assets, how they should be treated, and who should regulate them.

- Digital commodities: Assets like Bitcoin (and for some bizarre reason, Ethereum) would be classed as commodities (like oil and wheat) due to the fact they’re not operated or issued by any central entity.

This means they fall under the regulatory jurisdiction of the Commodities Futures Trading Commission (CFTC).

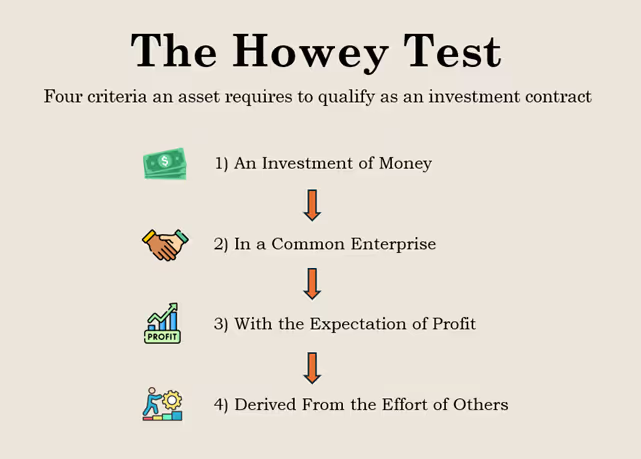

- Investment Contract Assets: These are typically tokens (aka shitcoins) where investors seek a financial return based on the efforts and success of the team who created the project.

In simple terms, if your token passes what is known as the Howey Test, then your token is a security, and you will be required to adhere to any reporting requirements set out by the SEC.

- Permitted Payment Stablecoins: The Clarity Act references the GENIUS Act to provide a framework for stablecoin regulation which dictates that stablecoins like USDT or USDC must be backed 1:1 by high-quality, liquid reserve assets like cash or US treasury bonds.

The aim is to make stablecoins more ‘stable’, to avoid seeing a repeat of TerraUSD, where Do Kwon’s dollar-pegged stablecoin became unpegged, crashed to 0, and wiped-out billions in investor funds.

2) The ‘Mature Blockchain Test’

You might think that this better categorization of digital assets would lead to more clarity, but that would be wishful thinking, because the Clarity Act also introduces something known as the ‘Mature Blockchain Test’.

The test is designed to introduce the concept of "mature blockchains" that have evolved into networks decentralized enough to no longer be controlled by any single person or group.

If the test determines that there are no special privileges for insiders, nobody owns more than 20% of the supply, and value is derived from real-world use, then a blockchain can be deemed “mature”, and its tokens can be traded as digital commodities instead of securities, and avoid oversight from the SEC.

3) New Rules for Middlemen

The Clarity Act also creates new CFTC registration categories for "digital commodity exchanges," "brokers," and "dealers”, covering basically any third-party business engaged in the buying, selling or custody of Bitcoin.

Under the proposed rules, these businesses must follow "core principles" like monitoring trades, keeping records, preventing manipulation, and segregating customer funds so they can’t be comingled.

Platforms like Coinbase, Binance, and OKX would all need to register to continue doing business in the US, and submit to tight controls, inspections, and data reporting requirements as set out by the CFTC.

4) Stronger AML and KYC regulations

No Government legislation would be complete without an intrusion into your privacy, and the Clarity Act doesn’t disappoint. The bill seeks to beef up anti-money laundering (AML) and know-your-customer (KYC) requirements for all intermediaries and mandates reporting on any “suspicious activity”.

The party line is that it’s all for your protection. The new rules will limit insider token sales, require full disclosures of project teams, and give regulators the power to delist ‘non-compliant’ assets to help tackle scams and rug pulls.

You can rest easy now anon, the government is here, and they definitely wouldn’t do anything nefarious with your data.

The Clarity Act – Latest Developments

The Clarity Act has been making its way slowly through Congress for the past 8 months, and everything was progressing smoothly with broad support from both industry representatives and both political parties.

This week however, everything changed. Upon reading the Senate’s alternative draft to the bill, Coinbase publicly pulled their support for the Clarity Act entirely.

The Senate’s alternative draft leans toward stronger SEC oversight and investor protections compared to the House-passed version which delegated more responsibility to the CFTC. The new draft enhances SEC authority over initial token sales, DeFi protocols, and stablecoins, including restrictions on yields and tokenized equities.

Coinbase are unhappy about this, because selling shitcoins and promoting yield products is big business for them. They want to continue offering yield on their stablecoin USDC, and given a choice, they would much rather operate under the more regulatory environment afforded by the CFTC.

The situation has become complicated, with a variety of vested interests all now pulling in different directions.

The American Bankers Association are in strong opposition to stablecoin yields for fear of mass deposit outflows from the banks, while stablecoin issuers like Coinbase argue that this is anti-competitive and protects the banks at the expense of the public. Meanwhile, Democrats like Elizabeth Warren are pushing for tighter SEC scrutiny in light of the FTX collapse, while Republicans like Cynthia Lummis want to see a CFTC commodity-like approach to foster innovation.

It's uncertain at this point what happens next, but if things remain stalled for too long it risks missing pre-midterm windows that would doom the bill’s ratification until at least 2027. The infamous shitcoiners Ripple, the VC fund a16z, and memecoin casino Kraken have all criticised Coinbase’s withdrawal of support, but Brian Armstrong remains resolute that they would rather have “no bill than a bad bill”.

Brian appeared in Davos this week to further promote his agenda. The place where all the people who have your best interests at heart tend to hang out…

Bitcoin Doesn’t Care – Should You?

It’s important to remember that while these politicians, bankers, and crypto middlemen all bicker and compete to build regulatory moats that further their own interests, the only relevant rules for Bitcoin are the protocol rules achieved through network consensus.

The state can create as many regulations as they like, but Bitcoin simply doesn’t care.

The more important question is, should you?

An important thing to notice amidst this debate is the framing of Bitcoin as a commodity and stablecoins as a medium of exchange. Both sides of the fence agree on that much at least.

But this, of course, is nonsense. Bitcoin is money. Peer-to-peer cash that frees you from the control of bankers, politicians and any other rent-seeking middleman. Is it any surprise they want to misrepresent Bitcoin in this way?

Brian Armstrong may be right that the banks are just trying to protect their own interests by preventing yield on stablecoins, but what he fails to point out is that these ‘payment’ products rely on you parking your wealth in dollar-pegged tokens that can be unilaterally frozen, surveilled, or censored at the drop of a hat. Don’t forget that just last week Tether froze the USDT owned by President Maduro at the behest of the US Government.

Do you really want to store your wealth in what is essentially a CBDC in disguise for a yield of just 3.5% APY? You’re not even beating inflation!

At an average 25% compound annual growth rate over the past 5 years, we’re happy to stick with Bitcoin in self-custody at 0% yield.

As for tokenised equities, we’ll let the speculators debate the merits, we’re only interested in sound money. Although it is worth mentioning that if it does come to pass, it’s likely to cause a lot of disruption for incumbents like the New York Stock Exchange (NYSE).

Ultimately, what we’re really witnessing here is a collection of politicians, bankers, and CEOs squabble over who gets to be in control of your money and what you’re allowed to do with it. If, like us, you don’t think any of them should be in charge, then you can simply hold your Bitcoin in self-custody and disregard their nonsense.

Bitcoin doesn’t care, and you don’t have to either.

Achieve True Clarity – The Bitcoin Way

If you use Bitcoin as intended, you don’t have to worry about any new rules these megalomaniacs come up with. There’s no need to fight the system; you can simply walk away from it.

Holding Bitcoin is a far better strategy for increasing your wealth than trying to chase yield on an evaporating currency, and preserving your sovereignty by holding it yourself is far safer than leaving it in the hands of unreliable middlemen.

What the government officials and third parties that are writing these new rules don’t want you to realize is that you don’t need them at all. Bitcoin allows you to grow your wealth and hold it securely without their involvement, and if you go to the effort of learning how to buy Non-KYC Bitcoin, you can even do it without their knowledge!

You can simply opt out and live a peaceful life.

When you’re ready to learn how to use Bitcoin to its full potential, our experts are on hand to walk you through everything step by step. You’ll be amazed how quickly your skills advance and your confidence grows.

To get started simply book a free 30-minute call and let’s get your first training session booked in.