Bitcoin Backed Loans - One Strike and You’re Out!

In this article:

Bitcoin is pumping once again, and for the 8th time in its history has breached the $100,000 mark. Excitement fills the air, FOMO is kicking in, and with calls for $1m per coin, the greed seeping back into the market is palpable.

With this boisterous energy returning, plenty of Bitcoiners will find themselves busy scrolling Zillow for their dream home, planning an exotic vacation or fantasising about that ’65 Mustang they have always wanted to own.

It’s a great time to be a Bitcoiner!

There’s nothing wrong with enjoying the rewards of our curiosity and discipline, but it’s helpful to remember that whenever you do start feeling like a genius, it’s probably time to stop and reflect. Pride often precedes a fall, and hubris can make you blind to risks you wouldn’t otherwise miss.

There’s a reason Bitcoiners repeat the mantra ‘stay humble, stack sats’.

So, this week, let’s take a look at one of those risks. A risk that has caught many a Bitcoiner offside in previous bull markets….

The Tradfi boys are back in town, and they are here to offer you Bitcoin backed loans.

Married to the Hodl, Desperate to Spend

Bitcoin bull markets are a wild ride, and even the most stoic amongst us find it hard not to get swept away with the excitement. Seeing your net worth skyrocket at a rapid pace is enough to make anyone a little giddy.

The problem is, it doesn’t do much good for our decision making. Weeks of extreme doses of dopamine and adrenaline will inevitably start to take their toll. If you’re not careful, it can lead you into making decisions you might not have, if you were thinking more clearly.

A particular dilemma that bull markets can create for Bitcoiners is having to sit and watch your net worth balloon while remaining true to the ‘Hodl’ mantra that enabled it. You’ve hardened the ability to delay your gratification, but it sure would be nice to upgrade your life a little.

If only there was a way to sell your Bitcoin without selling your Bitcoin….

Well, as you might expect, there are always people willing to cater to your every desire. Especially if it means getting to handle your Bitcoin. The bull market is back, and like clockwork, so are Bitcoin backed loans.

In this bullish environment, the idea of using your Bitcoin as collateral for a fiat loan can seem quite enticing. It almost looks like a cheat code. You get to keep hodling your corn without selling, but at the same time unlock a bit of cash to splurge or invest. What’s not to love? You could even buy more Bitcoin with it!

Maybe you can have your cake and eat it too….

Bull markets tend to breed a unique form of irrationality. As the price rips higher and FOMO kicks in, so does recency bias, a tendency to assume that recent price trends will persist indefinitely.

This skewed perception leads people to conclude that if Bitcoin trends higher forever, then any loan fiat loan taken against it will quickly become over collateralised, making it trivial to pay off the principal. Better yet, if you use the loan to stack even more Bitcoin, then your gains will easily negate any interest paid.

It’s an Infinite money glitch! A speculative attack on the dollar! We’re all Michael Saylor now!

What could possibly go wrong?

Well, quite a few things actually. Let’s explore them…

Bitcoin Backed Loans – The Risks & Drawbacks

Bitcoin backed loans come in all shapes and sizes. Some offered by traditional financial institutions in exchange for dollars in your bank account, and some offered by Defi platforms that will lend out stablecoins.

It would take too long to pick apart the trade-offs of each, so instead, we thought we would provide a helpful summary of all the potential risks you should consider before you dive into a Bitcoin backed loan of any type.

Leverage, Volatility & Liquidation Risk

Over the long-term, Bitcoin has always been on an upward trajectory. But look beneath the surface and you’ll see that its journey is littered with savage corrections, sometimes as deep as 80%. Even in bull markets corrections of between 30 – 40% are common.

One of the primary risks associated with Bitcoin backed loans stems from its price volatility. This is what the bull market looked like in 2017

Everyone loves explosive green candles in a bull market, but this volatility cuts both ways. The red candles can be just as dramatic. Bitcoin’s notorious volatility vs the dollar is what amplifies the risk of using it as collateral for a loan.

Bitcoin-backed loans typically require you to maintain a specific loan-to-value (LTV) ratio of 60% or lower. So, if you wanted to borrow $60,000, you would need to post $100,000 of Bitcoin as collateral. If the value of Bitcoin continues to rise, then your LTV ratio will trend steadily downward.

If however Bitcoin’s price drops sharply, by say 40%, then your LTV would quickly rise to 100%, and the value of your collateral would fall below the requirements set out in the terms of the loan. In this scenario, lenders will issue what’s known as a margin call. They will demand you post more Bitcoin to increase your collateral and shore up the loan. If you fail to comply, your Bitcoin could be liquidated, potentially wiping out your holdings.

We’re bullish on Bitcoin long term and have never been big fans of Keynes, but he was right when he said the market can stay irrational longer than you can stay solvent. If you are going to introduce leverage into your Bitcoin journey, then tread VERY carefully. Don’t over stretch yourself, or one sharp correction could cost you everything.

Counterparty Risk

As soon as you enter into a loan agreement using your Bitcoin as collateral, you’re introducing counterparty risk. By letting anyone else hold your Bitcoin as collateral you are trusting them to keep it safe and not lose it or steal it.

Misplaced trust in institutions has resulted in many a sad story for Bitcoiners over the years. Countless exchanges have gone under over the years and it’s a trend that is guaranteed to continue. ‘Not Your Keys, Not Your Coins’ is a mantra in the Bitcoin community for a reason and most people understand that giving anyone else access to your Bitcoin is an unforgiveable mistake to make.

These risks are far beyond theoretical. There are plenty of examples of companies offering Bitcoin backed loans blowing up and costing their customers billions of dollars collectively. If you’re considering a Bitcoin backed loan and haven’t read up about Voyager, Celsius and BlockFi, the three musketeers of getting their customers rekt, then you definitely should. It will definitely make you think twice.

Defi lending platforms aren’t necessarily less risky either. They might be decentralised, but borrowers are still only one smart contract bug or protocol exploit away from their collateral going up in smoke.

The point is, the second you let anyone else other than you have any level of access to your Bitcoin, you are increasing your level of risk.

Regulatory Risk

Handing your Bitcoin over to a regulated financial institution?

Welcome back to the Matrix.

You didn’t just give control of your Bitcoin to a trusted third party, you also put it within tantalisingly close reach of your government’s sticky fingers. That’s a bold strategy…

Regulated financial institutions will bend the knee instantly to demands from government. Their allegiance to you will last only as long as your incentives both align. If they have to choose between your interests and staying in business, they will always choose the latter.

This leaves you exposed to the whims of the state. Something Bitcoin was designed to protect you from.

Remember that in 1933 The US Government banned private ownership of gold and forced citizens to exchange it for dollars (which they promptly debased). What would stop the state working with financial institutions to appropriate your Bitcoin under the guise of ‘national security’? Would you be content never seeing your Bitcoin again and being offered stablecoins or the government’s new CBDC in exchange?

And the threat from the state isn’t limited to just confiscation. At any time the government can impose new taxes, reporting requirements, or restrictions.

Perhaps you trust your government. If so, God help you. For the more prudent amongst us, not considering these risks means you’re not taking this as seriously as you could be.

Interest Rates & Collateral Requirements

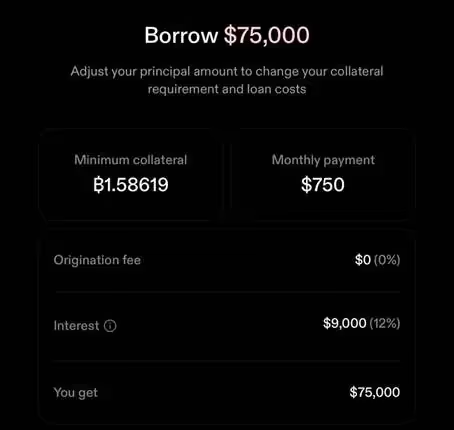

Bitcoin-backed loans often come with steep interest rates and high collateral requirements compared to traditional loans. Looking at recent offerings on the market we see providers like Unchained, Ledn and Strike offering rates of between 9 – 13% APR with a maximum LTV of 50%.

The first thing you notice about these products is the high collateral requirements. The minimum sized loan you can get through Jack Maller’s company Strike is $75,000 and would require an LTV of at least 50%. This means you have to pledge at least $150,000 worth of Bitcoin to access it.

Then there are the interest rates. Strike’s latest offering charges 12%, APR on these over collateralized loans. That is NOT what you would call ‘cheap debt’. The average national APY on an unsecured personal loan is only just over 12% meaning anyone with an average credit score could get the same APY from a bank but without having to provide any collateral at all.

Not to mention there are countless other ways to access debt without such high collateral requirements or interest rates. Credit Cards often offer 0% introductory offers or balance transfers, banks will offer you much more competitive home equity loans and even some pawn shops will give you 10%.

Most people in the position to service a loan as large as $75,000 probably have good enough credit to access far better financing deals and without having to add counterparty risk or leverage to their Bitcoin stack.

The only people these loans should appeal to are either fools or those with poor a poor financial history who want to avoid paperwork and credit checks.

Rehypothecation Risk

Rehypothecation is when a lender uses your Bitcoin collateral for their own purposes, like lending it out or trading with it to generate profit. It provides another potential revenue stream for lenders, which can lower interest rates, but it introduces significant risk.

If your lender overextends themselves or takes risks that don’t pay off, your Bitcoin could be tied up in their failed bets, making it hard or impossible to recover. Centralised platforms have been notorious for this in the past engaging in rehypothecation, often without clear disclosure.

Again, it would be wise to revisit the stories of Celsius, Voyager and BlockFi to see how quickly these types of firms can get into trouble, go bankrupt and take their customers down with them.

It’s easy to make money in a bull market, but when the tide goes out, Bitcoin quickly reveals who has been swimming naked.

Tax Implications

Another thing a lot of people fail to consider when taking a Bitcoin-backed loan is that depending on your jurisdiction, it can trigger complex tax consequences.

While the money you receive as a loan typically isn’t taxable, your Bitcoin collateral might be. In some countries using your Bitcoin as collateral can be treated as a taxable event if the lender sells or rehypothecates it and if your collateral is liquidated during a price dip, you could face capital gains taxes on the disposed Bitcoin, even if you didn’t profit.

In the U.S., the IRS treats Bitcoin as property, meaning any transaction involving it requires the appropriate reporting. If you fail to track these events properly it can lead to penalties or audits. If you’re found to be non-compliant then you could find yourself faced with unexpected tax bills, and invoices from the tax professionals you needed to hire to sort it all out.

If you want to play fiat games, you have to play by fiat rules. Unfortunately, they are not skewed in your favour.

HODL Responsibly – The Bitcoin Way

One of the most amazing things about Bitcoin is that it’s the ultimate bearer asset. If held in full self-custody it comes with zero carry cost, no counterparty risk, and zero risk of confiscation, rehypothecation, or liquidation.

Handing over the keys to your Bitcoin and giving up all these benefits to secure an over collateralised loan at uncompetitive rates is extremely risky business. You’re not copying the Michael Saylor ‘playbook’. MSTR raises debt at close to 0% interest. If you’re taking on debt to buy more Bitcoin at 12% then you’re trying to play the same game but with a severe disadvantage.

One way to avoid the allure of these potential debt traps is to recognise one inalienable truth. Despite what all the talking heads will tell you, Bitcoin is not an ‘investable asset’, It’s just a superior form of money. If your purchasing power has increased and you want to enjoy some of it, then you can just spend it and live within your means.

The only way for you to try and HODL your Bitcoin and spend it too is to introduce leverage and counterparty risk. When Bitcoin offers a 5 year CAGR north of 50% and rewards you handsomely for just holding it without any leverage, you have to ask yourself if trying to get the best of both worlds is just a symptom of greed. Perhaps you shouldn’t look a gift horse in the mouth.

If you’re more interested in hodling your Bitcoin responsibly, then that’s something we can help with. We teach you how to secure your Bitcoin for the long-term using only the very best open-source tools. No custodians, no counterparty risk and no compromises.

Start your training by booking a free 30-minute consultation today and we will make sure your Bitcoin journey is a smooth one.