Ownership Is Not the Same as Access

In this article:

For most people, the rules of money seem simple: if the balance is in your account, it’s yours, if you own an investment you can sell it, and if you want to move your money somewhere else you just send it.

At least, that’s the assumption.

But every now and then the financial system reminds people that those rules come with an asterisk.

The kind buried deep in the terms and conditions nobody reads, the clauses explaining that withdrawals can be limited, transfers can be blocked, and that the money in your account is yours… until the bank decides it isn’t convenient to return it.

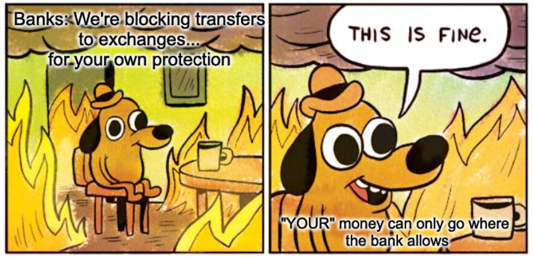

In the UK, several banks, including Barclays have introduced restrictions on transfers to Bitcoin exchanges. The justification is usually fraud prevention or customer protection. Whether you agree with the reasoning or not, the message is clear: the bank reserves the right to decide where your money can go.

None of it is even particularly unusual, but it does reveal something most people rarely think about. In modern finance, owning an asset and being able to access it are not always the same thing.

Most of the time transfers settle, withdrawals process, and markets remain liquid. Right up until they don’t. And when they don’t, the question that suddenly matters is a simple one: who is actually in control of your money?

Hint: it’s not the person whose name appears above the balance.

It’s the institutions that regard depositors the way a casino regards gamblers: welcome revenue sources, right up until they try to cash out.

A System Built on Confidence

To understand why access to money can suddenly become conditional, you have to understand how modern banking actually works.

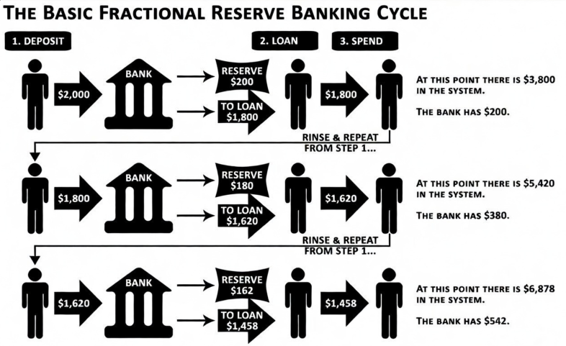

Despite the popular image of vaults filled with deposits, banks do not operate as storage institutions. They operate as credit creators.

When banks issue loans, they create new deposits in the process. The banking system expands money by expanding credit. The result is a financial structure in which the amount of money circulating in the economy is far larger than the reserves that support it.

This structure is often described as fractional reserve banking. In practice, the fractions have become increasingly small. In many jurisdictions, reserve requirements are minimal or even nonexistent.

What matters instead is confidence.

As long as depositors behave predictably, the system functions well enough to maintain the appearance of stability. Payments settle, loans are refinanced, and banks roll funding forward from one day to the next.

But that apparent stability rests on a simple assumption: most people will not try to withdraw their money at the same time. If they did, the system would struggle to accommodate them.

Banks and regulators know this. And the rules governing withdrawals, transfers, and liquidity are ultimately designed with that reality in mind. Which is why financial institutions tend to become particularly attentive whenever depositors start heading for the exit.

Think about it for a moment. Modern banking is a remarkable business model. Banks create money through credit, lend it out at interest, and use deposits as the fuel that keeps the machine running. When the bets pay off, the profits belong to the banks and their shareholders.

When the bets go wrong, the story tends to change. Losses are absorbed by central banks, governments, and ultimately the public, the same public whose deposits made the system possible in the first place.

In other words, the incentives are not exactly aligned with yours. The system works extremely well for the institutions running it.

The question is whether it works equally well for the people whose money keeps it alive.

When the Rules Change Overnight

Imagine waking up one morning to discover that the balance in your bank account has been cut in half.

Not because you made a bad investment, not because you were the victim of fraud, but because the banking system needed rescuing.

It sounds like the premise of a financial horror story. Well, in 2013, it happened in Cyprus.

For years the country’s banking sector had expanded aggressively, growing to several times the size of the national economy. Cypriot banks had filled their balance sheets with loans and large holdings of Greek government bonds, which appeared safe until Greece’s debt crisis forced massive losses across the region’s financial system.

When those losses surfaced, the banks were effectively insolvent.

Because nothing says "rock-solid banking" like expanding to seven or eight times the national economy on promises from a country already quietly circling the drain.

European authorities agreed to a rescue package, but the bailout came with a new condition. Instead of relying entirely on taxpayers, the banks would be recapitalized using the deposits already sitting inside them.

Two institutions sat at the centre of the crisis: Laiki Bank and Bank of Cyprus.

Laiki Bank was dismantled. Deposits above €100,000 were frozen and ultimately wiped out as the bank was wound down. At the Bank of Cyprus, uninsured deposits were forcibly converted into shares to rebuild the bank’s capital base. Many savers lost roughly half their balances overnight.

At the same time, strict capital controls were imposed across the country. Banks closed for nearly two weeks. When they reopened, withdrawals were limited to €300 per day. Transfers abroad were restricted and businesses struggled to move money between accounts.

For the first time inside the eurozone, depositors were confronted with an uncomfortable reality.

The money in their accounts had not simply been “stored” by the bank. When the system needed rescuing, those deposits became part of the rescue.

Liquidity Is an Illusion

Cyprus was a visible reminder of a deeper feature of modern finance: liquidity is often assumed, not guaranteed. But of course, Cyprus was just a one-off.

A small, contained crisis in a peripheral economy. Nothing that could happen in the “civilized” Western financial system. It wasn’t.

In 2022, a very different kind of stress revealed the same dynamic in the United Kingdom.

When government bond yields moved sharply, a number of pension funds using liability-driven investment strategies suddenly faced large margin calls. On paper, these funds held billions in assets. In practice, they needed cash immediately.

And guess what? They couldn’t get it.

To raise liquidity, funds were forced to sell assets into a falling market, pushing prices down further and triggering even more margin calls. The situation escalated quickly enough that the Bank of England stepped in to stabilize the market.

Ah yes, the noble central bankers ride to the rescue. Those selfless guardians of stability, firing up the money printer to "save" the system they themselves rigged into fragility. Because nothing screams capitalism like unelected bureaucrats conjuring billions out of thin air to bail out leveraged pension funds holding "risk-free" government bonds that suddenly aren't liquid enough when it counts.

The same principle appears across large parts of modern finance.

Many investment funds promise periodic liquidity to investors while holding assets that cannot easily be sold on demand. Under normal conditions, this mismatch goes unnoticed. Until it doesn’t.

In recent months, investors in private credit funds linked to firms such as BlackRock and Morgan Stanley have encountered this reality. When redemption requests surged, withdrawal limits were activated. Investors could request their money back but only within predefined thresholds, and only on the fund’s terms.

When Access Can Be Switched Off

What if you don’t even get the option to withdraw? What if the system doesn’t force you to sell, but simply prevents you from transacting altogether?

That possibility is no longer theoretical.

In 2022, during the trucker protests, authorities in Canada instructed financial institutions to freeze accounts linked to the demonstrations. Individuals who had not been charged with a financial crime found themselves unable to use their bank accounts, without prior notice and with limited immediate recourse.

The balances remained visible. But access, including the ability to spend, transfer, or withdraw, had effectively been removed.

This was not a failure of liquidity, nor a breakdown of markets. It was a policy decision, implemented through the existing financial infrastructure.

And that distinction matters.

It shows that in a system where money exists primarily as entries on institutional balance sheets, access is not just governed by markets or contracts, but also by rules, authorities, and discretionary decisions made above the level of the individual user.

Whether one agrees with the specific circumstances or not is beside the point. What matters is what the episode revealed.

Financial access can be restricted quickly, and in ways that leave the underlying balances intact but unusable.

The direction of travel suggests this layer of control is unlikely to diminish. Central banks, including the Bank of England, are actively exploring digital currencies designed to operate entirely within centrally managed systems.

The Common Thread: Counterparty Risk

What ties these events together is not geography or policy, but structure.

In each case, access to money depends on an intermediary. A bank holds deposits, a fund manages assets, a clearing system settles transactions, and a regulator ultimately defines the rules under which all of this operates. As long as those layers function as expected, the system appears stable and predictable.

But that stability rests on a dependency that is easy to overlook.

Your ability to access and move your money is contingent on the institutions that sit between you and it, their solvency, their constraints, and, at times, their discretion.

This is what is meant by counterparty risk.

It is not simply the risk that an institution fails. It is the risk that, under pressure, the terms of access change. As we saw, that pattern has already appeared in different forms.

In Cyprus, depositors discovered that their savings could be used to recapitalize the banking system. In the United Kingdom, pension funds discovered that contracts and counterparties could force them to act on a timeline not of their choosing. In Canada, account holders discovered that access to their balances could be restricted altogether.

Just a few weeks ago, investors in private credit funds linked to BlackRock and Morgan Stanley were reminded of the same underlying reality. When redemption requests surged, withdrawals were capped under the terms of the funds. BlackRock’s HPS Corporate Lending Fund limited redemptions after requests exceeded its quarterly threshold, while a Morgan Stanley private credit vehicle fulfilled only a fixed proportion of withdrawal requests (around 5% of fund units) despite higher demand.

This time no emergency powers were invoked, and no rules were broken. The system operated exactly as designed, and access to capital was still constrained when it mattered most.

Different events, but the same underlying structure.

The more layers stand between you and your money, the more conditional your control becomes.

The Alternative

For most of modern history, there was no real alternative.

If you wanted to store value, you used a bank. If you wanted to invest, you relied on financial institutions. If you wanted to move money, you did so through systems designed and controlled by others. Participation in that system wasn’t a choice so much as a requirement.

And for a long time, that arrangement was simply accepted. Not because it was perfect, but because it was the only game in town.

Bitcoin represents a different approach. Not a refinement of the existing model, but a departure from it.

Bitcoin is not a claim on a bank or a fund, and it does not depend on a balance sheet or an intermediary to exist. It is a bearer asset, controlled through private keys, and transferable without requiring permission from a third party.

That distinction is subtle in stable conditions, when the system functions as expected. It becomes far more meaningful when access is restricted, delayed, or denied.

Of course, holding Bitcoin directly introduces responsibilities that the traditional system has long abstracted away. Custody, security, and operational understanding become part of the process rather than services provided by an institution.

This is precisely the gap that The Bitcoin Way is designed to address: helping individuals move from passive exposure to active ownership, and to do so with a clear understanding of both the risks and the responsibilities involved. If you want to do this properly, you can book a free 30-minute consultation with one of our experts.

We’ll guide you through building a setup that’s secure, understandable, and fully under your control.

Because the real shift is not simply from one asset to another, but from a system where access is mediated and conditional, to one where ownership is direct.