Bitcoin and the Death of Consumerism

In this article:

In 2024 you don’t have to look far to find evidence to suggest that modern society is plagued with a zeitgeist of instant gratification, rampant consumerism and with it, plummeting standards of living.

In modern society, convenience and speed are king. The food is fast but lacks meaningful nutrition. Clothes are cheap and change every season, but are not made to last. Even the timber for new build properties comes from rapidly grown trees, but at the expense of quality and strength. The result is a society that despite having more advanced technology than prior generations, finds itself consuming lower quality goods and doing so more frequently.

Once you notice this trend, you begin to see this slow degradation everywhere. Supermarkets offer lower quality food, but much more of it. Flat pack furniture is quick and convenient, but is flimsy and needs replacing more often. You can fill your wardrobe very cheaply, but the clothes you buy won’t survive more than a handful of washes.

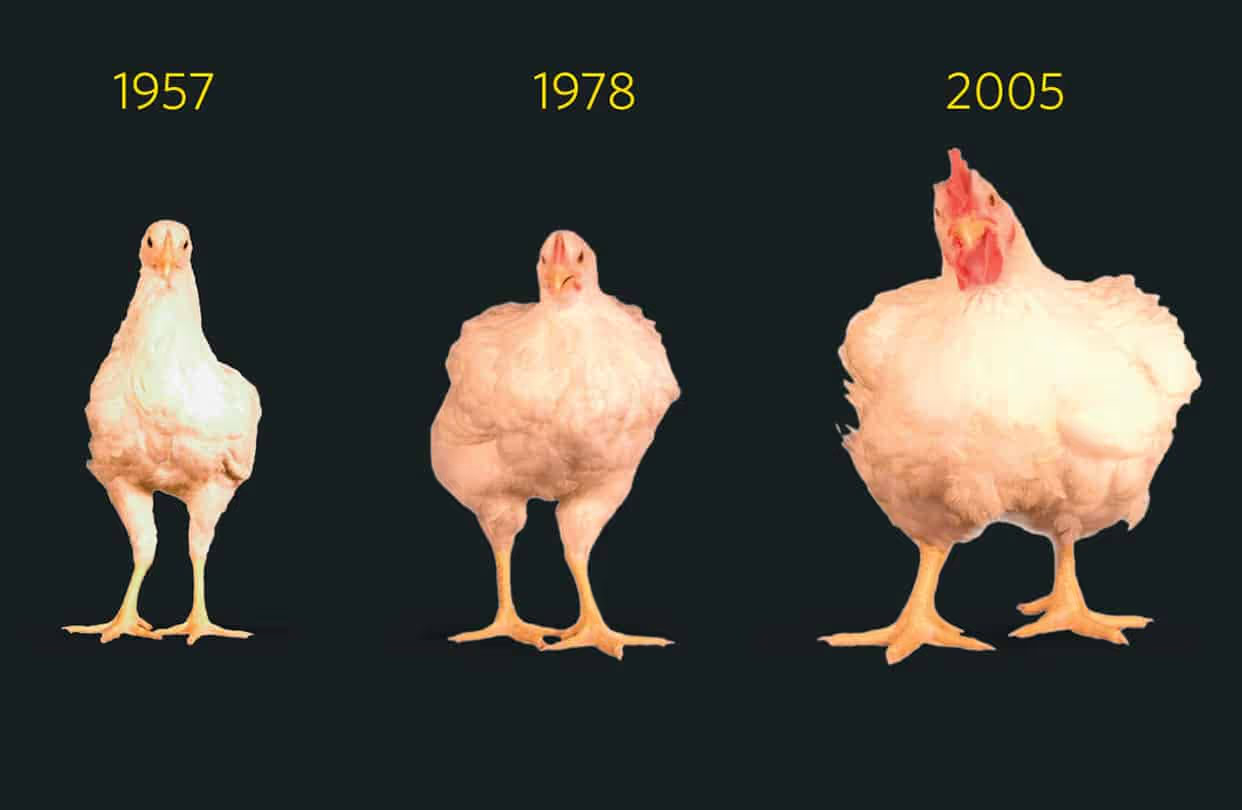

Experienced carpenters will tell you to seek out old tools because the alloys made to construct them were tougher and better quality. Your grandmother will tell you how her old vacuum cleaner still has the suction of a black-hole and that household appliances used to last decades. Builders know better than to live in houses built less than 30 years ago. You might even find a retired chef who tells you that once upon a time, chicken had a beautiful flavour all its own. Unlike today’s chicken, bred for speed and size alone that’s so bland it can’t be enjoyed without some sort of sauce or seasoning.

Everywhere you look, the race to the bottom is on. But who fired the starting gun? What on earth is going on?

Speed and convenience have value, but surely not at the total expense of quality and longevity. It can’t possibly be more economically viable, practical, or even desirable for consumers to buy low quality goods and need to frequently discard and replace them. How is it that goods and services are declining in quality over time whilst also constantly increasing in price? Surely with advances in technology, the inverse should be true, shouldn’t it?

Let’s explore these questions in pursuit of a common denominator that drives this phenomenon. Are there incentives at play that aren’t immediately obvious? Why does ‘frequency of consumption’ seem to trump ‘quality of consumption’?

If Consumerism is the Symptom, Central Banking is the Cause

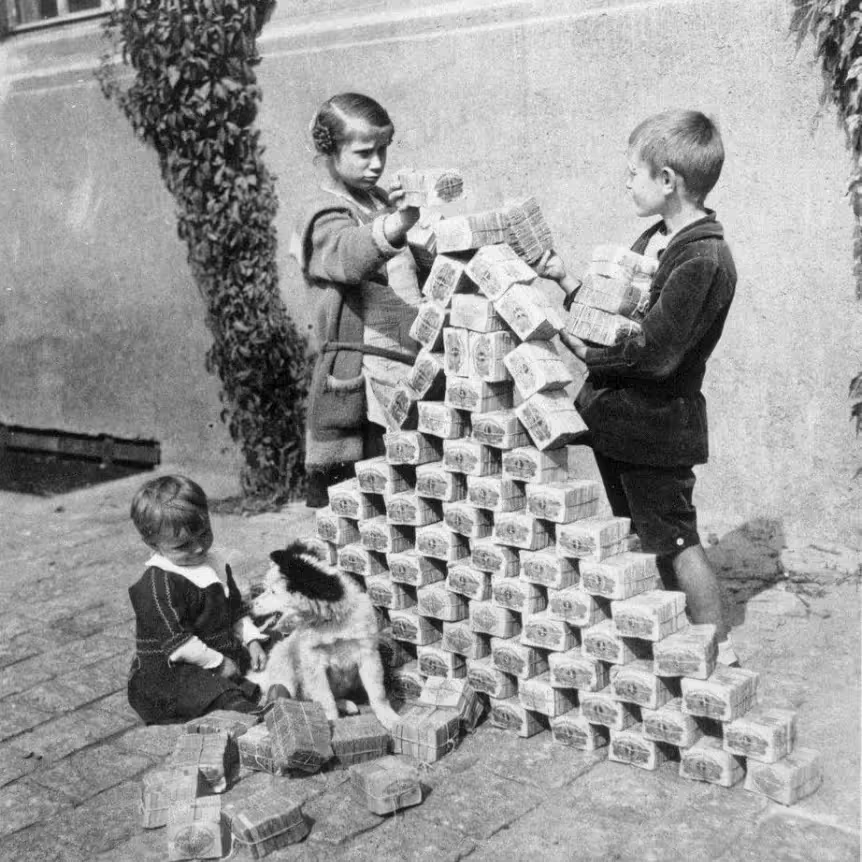

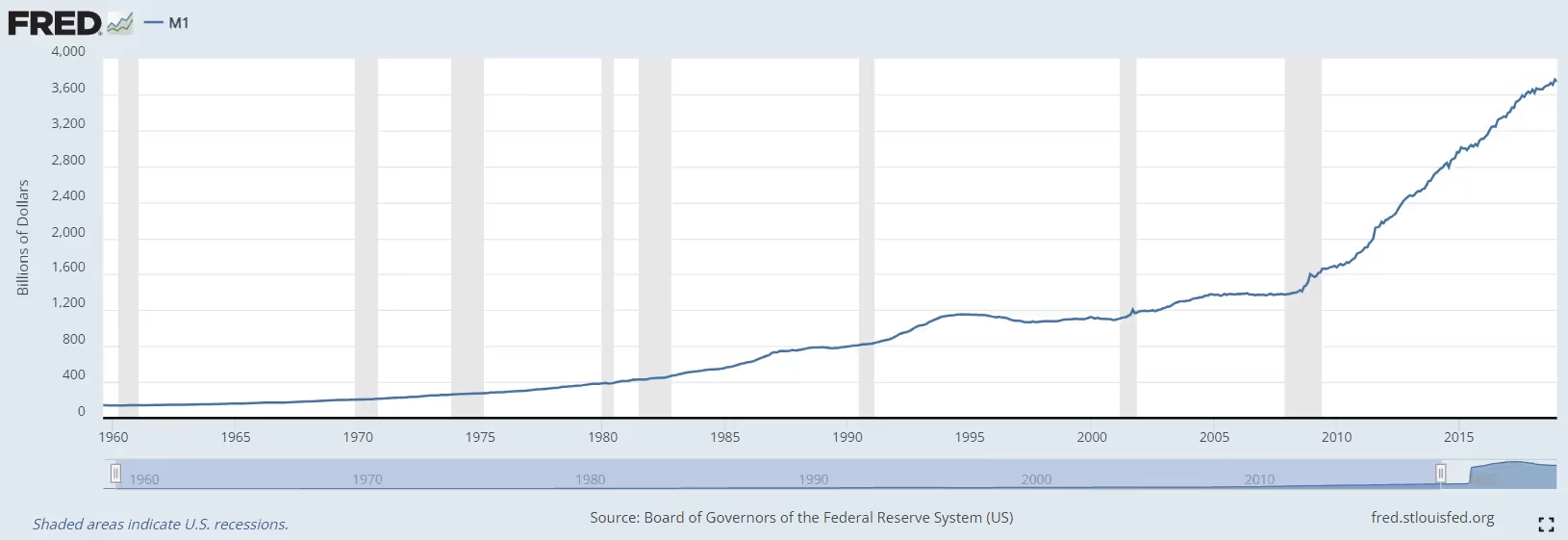

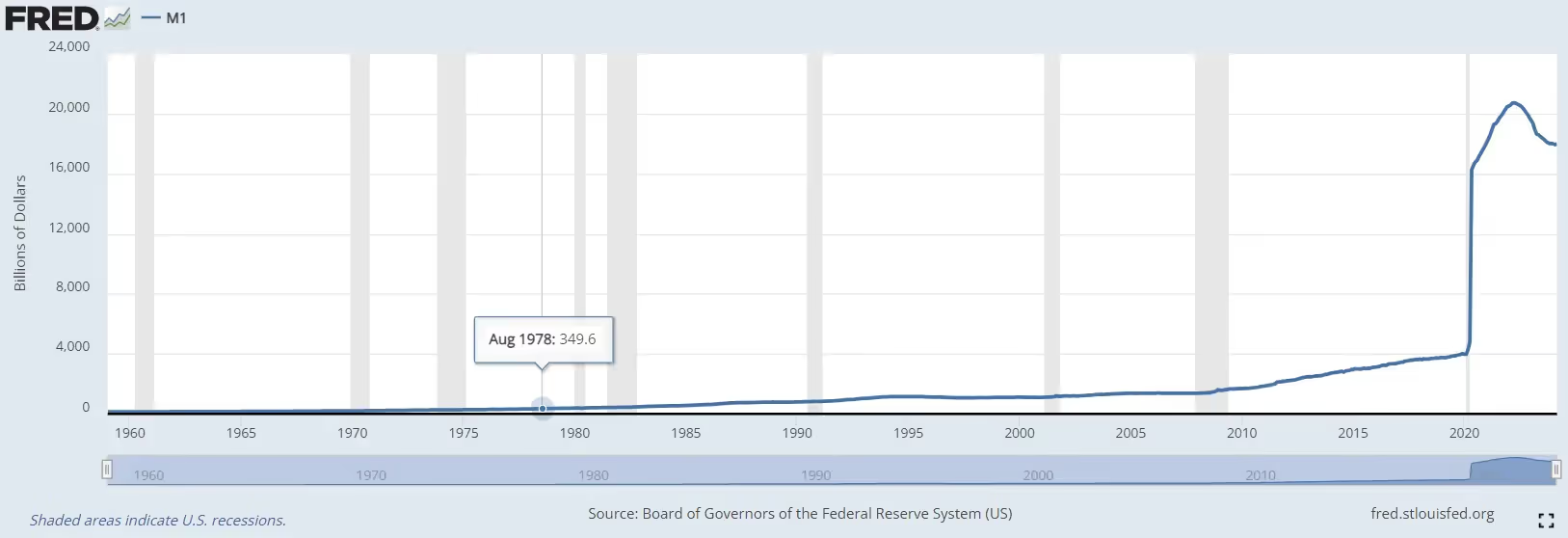

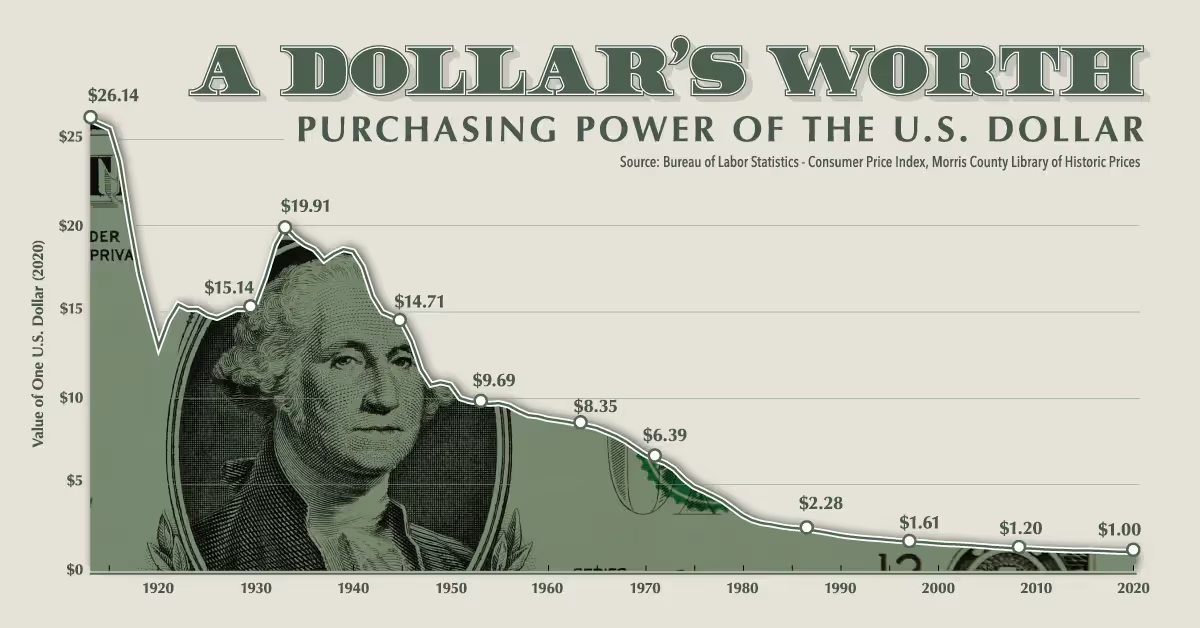

By now I doubt you need to be reminded that for the past 50 years Governments all over the world have been in the process of printing their national currencies into oblivion. The Federal Reserve’s own data shows that between 1959 and 2019 there was dramatic growth in the M1 Money supply ($). Since Nixon renounced the gold standard in 1971 and up until 2019, the circulating supply of US dollars exploded by a staggering 1600%! (No, that’s not a typo)

As if that wasn’t terrifying enough, look at what then happened between 2019 and today. If you thought a 1600% increase in 48 years was alarming, how do you feel about a further 380% increase from there in just the past 5?

Yikes! This means the total amount of US Dollars in circulation has increased by a mind bending 8,252% since 1971. These numbers aren’t just shocking, they are utterly absurd! It turns out inflation was never ‘transitory’, in fact, it was just getting started!

Most of you will already be painfully aware of the consequences of this huge expansion in money supply. As central banks create and inject more money into the economy, the total supply of money increases relative to the goods and services available to buy with it. Simple supply and demand dictates that the prices of these goods and services must therefore rise. If you stop to appreciate that the money supply has grown over 8000% in just the past 50 years, you can start to comprehend why fiat currencies have seen their value decimated so severely. The graph above highlights why this has been particularly noticeable in the past 5 years. Prices aren’t rising, the value of your money is haemorrhaging.

We’re probably not telling you anything particularly new here. You were already aware that inflation of the money supply causes its value to decline and prices to rise. But why exactly does this explosion in the money supply lead to a society plagued by the pursuit of instant gratification derived from the consumption of low-quality products and services?

Wonky Money Creates Wonky Incentives

One of the core functions of money is to act as a reasonable store and measure of value. At its core, money serves as a repository for the value you create via your labour and production. By using money as a conduit for measuring and storing value, it allows you to save the fruits of your labour for later consumption or investment.

Money solves an important problem then. Without a vehicle to store the value of one’s labour, society would be left with inefficient barter being the only viable means of exchange. Money is simply a technology that solves this problem and allows us to delay our consumption for a time that is most convenient to us.

The issue we are now currently facing is that rampant inflation degrades this core function of money. when a currency inflates by over 8,000% in 50 years and then begins rapidly accelerating, it can no longer serve as a reliable store of value or consistent measuring stick. It creates a world of wonky incentives and in worst-case scenarios, you might find yourself in living in a society reminiscent of 1923 Weimar Germany.

We’ll save exploring the ravages of what extreme hyperinflation did to Weimar Germany for another article. Instead, we want to demonstrate that even before reaching these cataclysmic failures, even subtle but persistent debasement of the money supply creates undesirable incentives that have profound effects on individual behaviour and society at large.

The Insidious Nature of Inflation

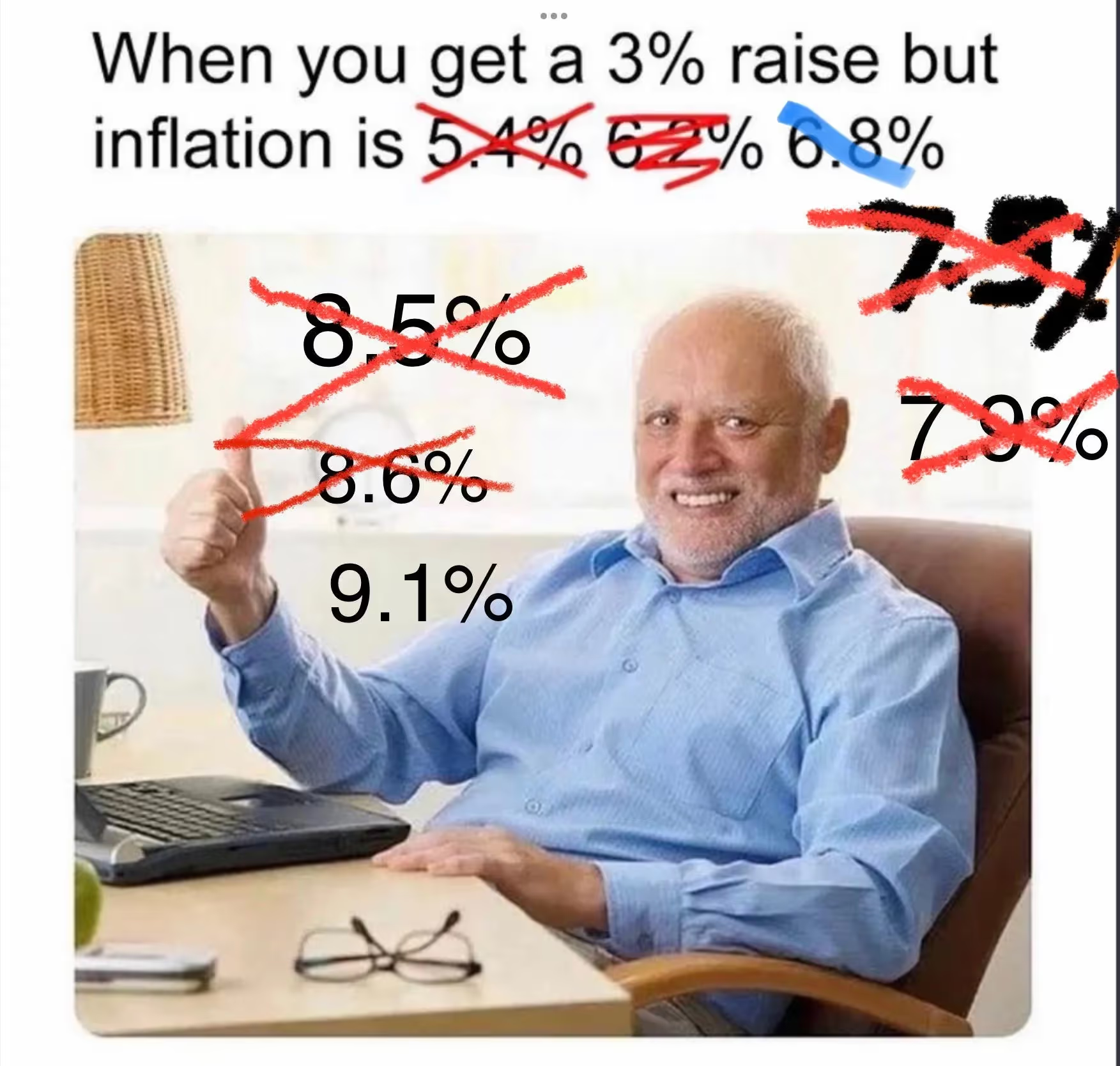

When your money is continually losing purchasing power it completely disincentivises saving and long-term financial planning. For example, let’s say you have $10,000 saved and plan to hold onto it for 10 years. If inflation during that period runs at 9%, then after those 10 years your £10,000 would only maintain the equivalent purchasing power of $4,224. Your purchasing power dropped by 57%!

Those who might accuse me of cherry-picking high rates of continued inflation to illustrate my point would be right. So, in the balance of fairness I should also point out that at the FED’s target rate of 2% inflation, your $10,000 would only maintain a purchasing power of $8,203. Even at the FED’s targeted rate of debasement, your savings will still decline in purchasing power by a staggering 18%!

It would seem then that the adage ‘Save for your future’ isn’t such sage advice anymore. In fact, you could even argue that with this new incentive in play, it looks more rational to consume your money as soon as possible before it can be exchanged for less! With inflation eroding the value of money over time, a clear incentive is set that sees people prioritise immediate consumption. Sure, they could invest spare earnings, but they would need these investments to consistently outpace inflation to make any progress. To suggest everyone must now earn a living AND manage a successful investment portfolio just to achieve a reasonable standard of living is simply not a realistic proposition.

For those lucky enough to have already accrued wealth, the name of the game is now preservation. Storing wealth in cash is not a viable strategy without facing a significant erosion of purchasing power. So instead, inflation forces these people to have to speculate and gamble simply to stand still. Even if inflation runs at only 2% per annum, they need to find returns of 18% each decade just to tread water. Welcome to the Hotel California, you can check out any time you like, but you can never leave.

For younger generations the situation is far more dire. Without sound, stable money to use as a vehicle to save for their future, there is simply no way for them to feasibly accrue meaningful wealth. Apart from anomalies like YouTube stars and a very small percentage of top earners, young people face an almost impossible task. The notion that the average salary would allow them to build enough wealth to own a home and raise a family has become nothing more than a fairy tale. The result? Nihilism, and in the absence of any opportunity for delayed gratification, wanton consumerism and short-term decision making.

So, if you ever find yourself guilty of thinking that younger generations are lazy and lack motivation, consider how you might feel if you were in the same position. Imagine joining a game of Monopoly halfway through. All the property is already taken, and you just go round and round the board trying to collect $200 for passing go and only try to survive. Think you’d still want to play? Probably not. You’d probably change your gender, start an OnlyFans page and head to Coachella too. YOLO!

Debasement of a society’s currency results in the debasement of society itself. The kids aren’t alright.

Crappy Incentives, Crappy Products

OK, the incentives are in place, the hunt for instant gratification is on and the name of the game is consumption. But why has this shift in incentives caused the quality of goods and services to decline over time? This topic alone could be discussed in some detail, but instead we’ll leave you with just a couple of points to consider.

First, ask yourself whether a consumer driven by immediate satisfaction is likely to be a discerning one. When consumption is undertaken purely for the sake of it, the propensity of that consumer to care about quality is diminished. Their goal is more focussed on the act of purchasing rather than making a considered investment.

For these consumers, frequency of consumption trumps quality of consumption. The monetary incentives driving their behaviour means they would rather buy ‘cheap’ low-quality clothing frequently, instead of high-quality clothing infrequently. Understandably, the market responds to this, and you see the emergence of things like ‘fast fashion’. The irony of all this is that the consumer likely spends more overall replacing cheap clothes than they would if they bought high quality clothes that lasted longer. But who cares? What are they going to do with the money they save anyway? Keep the cash in the bank for a rainy day? We already established there is no real incentive to do that. Don’t you get it? We’re YOLOING over here!

Second, consider that companies operating in this kind of environment are also at the mercy of inflation. Cost increases leave businesses in a tricky situation. Do they pass these additional costs through to an already overstretched consumer and face losing sales or do they accept lower margins? Given that neither of these outcomes is desirable, companies first look at ways to cut cost. This will typically include using cheaper materials, simpler manufacturing processes or less stringent quality control standards. Anyone else get nervous flying with Boeing these days?

When you apply first principles it’s easy to see the morass inflicted on society by the debasement of money. Keynesian economists would call this article hyperbolic. Perhaps they haven’t yet noticed that people are now buying Big Mac’s on credit. Can’t afford what barely passes for a burger these days? Fear not! You can pay for it in three easy instalments! CONSUME!

Bitcoin – The Death of Consumerism

The emergence of Bitcoin hails the end of this destructive journey into the abyss of consumerism. By adopting Bitcoin, society can put an end to the constant debasement of money and its inevitable degradation of our society. Bitcoin has the potential to achieve this because it fixes the wonky incentives that fiat currency created.

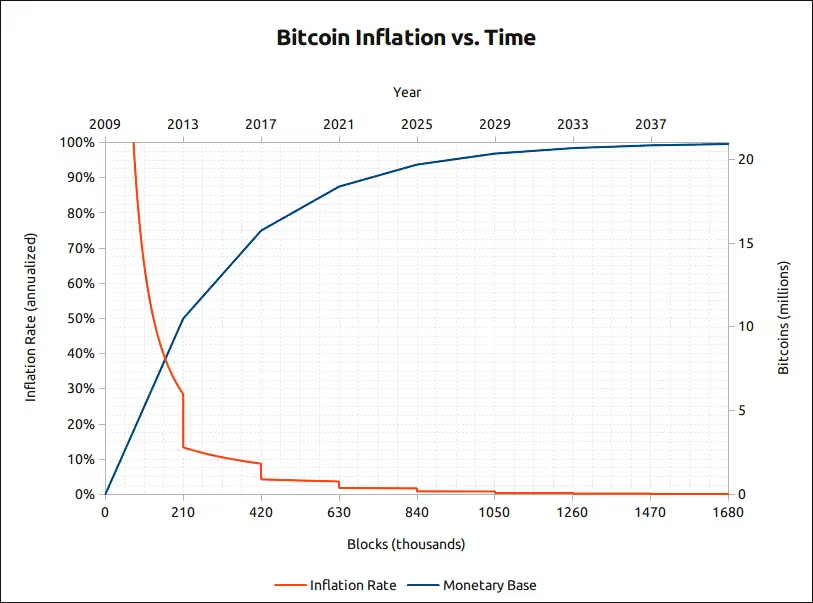

Fiat currency is debased at the whim of central banks and Governments. Their addiction to using this hidden form of taxation to enrich themselves at the expense of the rest of society is the root cause of the mess we currently find ourselves in. In stark contrast, Bitcoin’s inflation rate is entirely predictable and programmed to decrease over time, and this results in a fixed cap of how many Bitcoins will ever exist. This feature is hard coded into Bitcoin’s protocol which means that no powerful interests can change the supply without the consensus of all participants on the network. Where the circulating supply of fiat money is inherently unpredictable and unstable, Bitcoin’s is 100% predictable and measurable.

The introduction of sound money, free from the scourge of debasement, holds profound implications for society. Bitcoin’s emergence brings with it a new set of incentives and finally offers people a reliable monetary instrument that they can use to accumulate wealth. Where fiat currency encourages nihilism, instant gratification, and consumerism, Bitcoin acts as an invitation to instead postpone gratification in pursuit of a better financial future.

It wouldn’t be wise to underestimate how powerful the draw of this new incentive is. It reshapes everything. People who save in Bitcoin are unlikely to part with it easily, and for good reason. They know two important things. First, they know that deferring consumption today now result in increased purchasing power in the future. Second, they know that Bitcoin is finite and not easy to acquire, and that it won’t be getting any easier. They realise that acquiring the same amount of Bitcoin in future will require them to exchange more of their labour for it than would need to be exchanged today.

The result? People who hold Bitcoin become discerning consumers with longer time horizons. When the incentive to defer gratification is strong, consumption becomes more considered. The rules of engagement have changed. If a company wants to convince people to part with their hard-earned Bitcoin, they had better make sure their product or service focusses on quality and provides true value.

Bitcoin represents the light at the end of the tunnel for all of us.

Already wealthy? Great! You can now protect that wealth without being forced to speculate and gamble to avoid the constant erosion of your savings. You don’t need to play these stupid games anymore. (Financial advisors, it might be wise to retrain).

Not wealthy yet? No problem! You now have a monetary vehicle that gives you the ability to safely store the fruits of your labour, delay your gratification and plan for your future. You might even find you think twice about splurging on that low quality fast-food. Afterall…. Wouldn’t it be cheaper, tastier, and more nutritious to just make your own? The bonus of course is that you now have a way to store the money you saved and grow your wealth!

Bitcoin heralds the death of nihilistic consumerism and all of us stand to benefit. By removing the wonky incentives of fiat currency Bitcoin ushers in a new meritocracy where hard work is properly rewarded, and the spoils go to those who provide the most value. For the first time in a long time the incentives are in place for you to build a future of wealth and abundance.

The only question that remains is, what are you waiting for?

Start Building Your Future

Thanks for reading folks. Hopefully this week’s article has inspired you to consider building your future on a Bitcoin standard rather than enduring the malaise created by the infinite supply of Government coupons.

If it has, but you feel like you need a little help getting to grips with Bitcoin then that’s exactly what we’re here for. Our experts can teach you everything you need to know about buying, using, and storing Bitcoin securely.

Life is better on a Bitcoin standard. Come and join us.